Futures Market: Overnight, LME copper opened at $9,160.5/mt, initially declined to a low of $9,107.5/mt, then fluctuated upward to a high of $9,170/mt before closing at $9,164/mt, with open interest at 280,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,500 yuan/mt, fluctuated widely to a low of 75,360 yuan/mt, then rose to a high of 75,750 yuan/mt before slightly retreating to close at 75,670 yuan/mt, up 0.33%, with trading volume at 17,000 lots and open interest at 150,000 lots.

【SMM Copper Morning Brief】News: (1) Due to a decline in food costs and stable service prices, the US December PPI unexpectedly fell short of expectations, potentially easing concerns about persistent price pressures. However, it is worth noting that the YoY growth rates of December PPI and core PPI both marked the largest increases since early 2023. (2) In China, December's new social financing and new RMB loans both rebounded, with the decline in M1 narrowing, the growth in M2 expanding, and the M2-M1 gap narrowing.

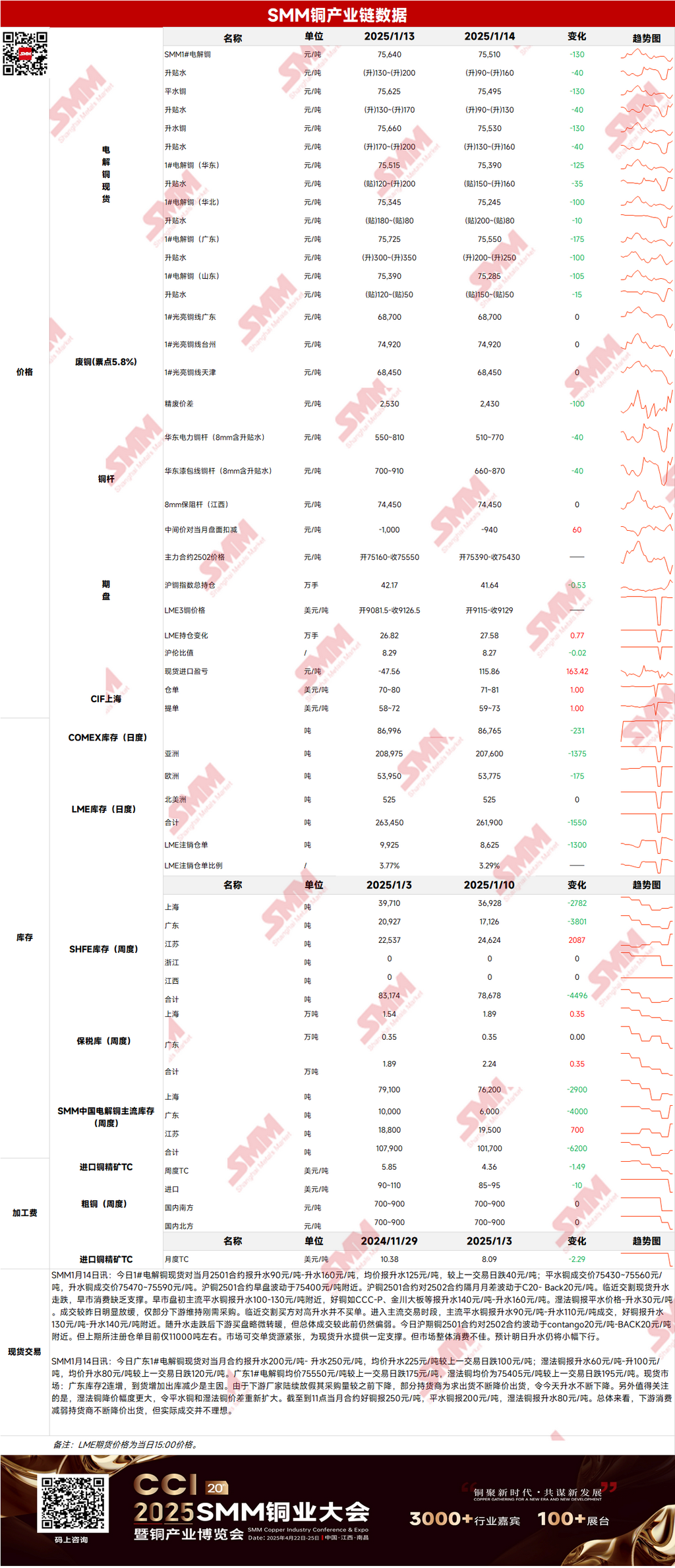

Spot Market: (1) Shanghai: On January 14, #1 copper cathode spot premiums against the front-month 2501 contract were quoted at 90-160 yuan/mt, with an average of 125 yuan/mt, down 40 yuan/mt MoM. Yesterday, the SHFE copper 2501 contract traded against the 2502 contract in a contango of 20 yuan/mt to a backwardation of 20 yuan/mt. However, SHFE registered warehouse warrants currently stand at only around 11,000 mt. Tight deliverable supply provided some support for spot premiums, but overall market consumption remained weak. Spot premiums are expected to decline slightly today. (2) Guangdong: On January 14, #1 copper cathode spot premiums against the front-month contract were quoted at 200-250 yuan/mt, with an average of 225 yuan/mt, down 100 yuan/mt MoM. Overall, downstream consumption weakened, and suppliers continued to lower prices to sell, but actual transactions were not ideal. (3) Imported Copper: On January 14, warehouse warrant prices were $71-81/mt, QP January, with an average up $1/mt MoM; B/L prices were $59-73/mt, QP February, with an average up $1/mt MoM; EQ copper (CIF B/L) was quoted at $9-23/mt, QP February, with an average up $3/mt MoM, referencing cargoes arriving in late January and early February. The SHFE/LME price ratio slightly improved yesterday. February long-term contract declarations gradually started, and early market offers slightly rose compared to the previous day, with EQ copper quotes remaining firm. (4) Secondary Copper: On January 14, secondary copper raw material prices remained unchanged MoM, with Guangdong bare bright copper prices at 68,600-68,800 yuan/mt, unchanged MoM. The price difference between primary metal and scrap was 2,430 yuan/mt, down 100 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,580 yuan/mt. According to the SMM survey, secondary copper rod enterprises currently adopt three procurement pricing methods: tax-exclusive, "reverse invoicing," and tax-inclusive. With the rise in copper price centers, secondary copper rod enterprises reported difficulties in pressing purchase prices and avoided stocking excessive raw material inventories before the Chinese New Year, aiming to convert all materials into finished products. (5) Inventory: On January 14, LME copper cathode inventories decreased by 1,550 mt to 261,900 mt; SHFE warehouse warrant inventories decreased by 1,355 mt to 9,730 mt.

Prices: Macro side, the US December PPI data fell short of expectations, the US dollar index slightly declined, and crude oil continued to rise, all supporting copper prices. On the fundamentals side, SHFE registered warehouse warrants currently stand at only around 11,000 mt, with tight deliverable supply providing some support for spot premiums. However, from the consumption perspective, as the year-end approaches, overall market consumption remains weak. In summary, with the US dollar index declining and crude oil continuing to rise, copper prices are expected to remain supported at the bottom today.

》Click to View the SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only and does not constitute direct investment research advice. Clients should make cautious decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】